"The Most Valuable Holiday Gift...?" - An Interesting Loophole for Teens and RothIRAs

I saw an interesting article this morning from Investopedia (always a favorite) about a tax loophole I was not aware of. While not an area of focus (particularly since my wife and I have no kids), I thought this would be an interesting (and QUICK) post for today in case you are interested in following the links for more information.

Article by Sabrina Karl at Investopedia - "Did Your Kid Earn a Paycheck This Year? This Could Be the Most Valuable Holiday Gift You Give":

As I mentioned above, I saw this article in my e-mail feed this AM. While I use Investopedia's resources regularly for PD sessions and as a link for teachers, I've increasingly been enjoying their daily articles on personal finance topics like this. Some are repeating financial advice I already know, but particularly in the world of investing I learn new things regularly. If you have never signed up for their articles, go to Investopedia (linked), pan down to the bottom of the main page, and click on the blue box labelled "Newsletter Signup" (the "Daily" is this one).

So let me start with a couple of interesting quotes from the article to (hopefully) get your attention . . .

"Once a teen has earned income from a part-time or summer job, they’re eligible to contribute to a Roth IRA—and this can create a unique tax advantage most adults can’t match. Why? Because Roth IRA contributions are made with after-tax dollars. For adults, that means choosing to “pay taxes now” in exchange for tax-free withdrawals down the road. But many teens earn so little that their federal tax rate is 0%, meaning they can put money in a Roth IRA that’s already tax-free."

Or this quote, "If your child has earned income, anyone in their life can contribute to their Roth IRA—grandparents, aunts, uncles, even a godparent. The only limits are the child’s total earned income for the year or the overall annual IRA contribution limit, whichever is less. . . for 2025, the IRS limit is $7,000—or your child’s total earned income for the year, if it’s less. That means a teen who made, say, $2,500 at a part-time job (paycheck income only—cash gigs like babysitting or lawn mowing don’t count) can contribute up to $2,500 to a Roth IRA for 2025."

Here are a few "rules" to keep in mind with this opportunity:

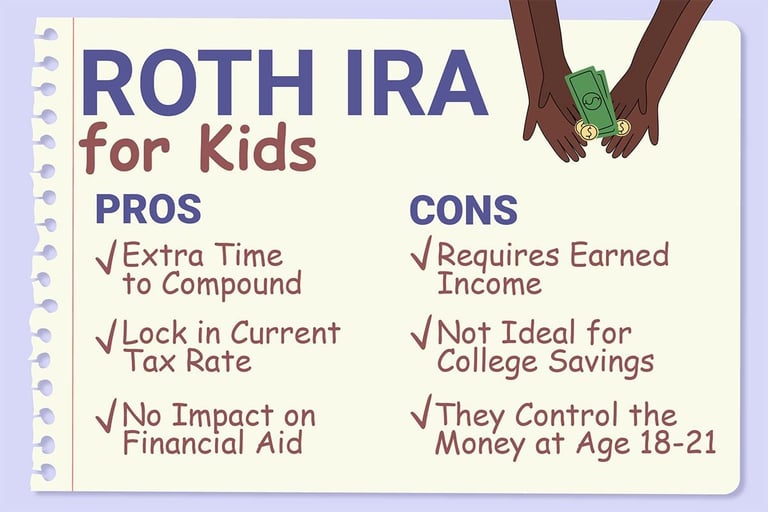

Earned Income is Mandatory - The minor must have income from work they performed, such as a part-time job (W-2) or self-employment (babysitting, lawn mowing, modeling, etc.). Allowance or investment income does not count. It is essential to keep records of cash-based income in case the IRS asks for verification.

Adult Controls Account until 18-21 - The account is opened in the minor's name with an adult as the custodian. There's no minimum age to open a Roth IRA for a child, just the earned income requirement. The custodian makes all investment and management decisions until the child becomes a legal adult, at which point full control transfers to them.

Withdrawal Flexibility - A key benefit of a Roth IRA is that the original contributions can be withdrawn at any time, for any reason, without taxes or penalties. NOTE that withdrawing the earnings early generally incurs both income tax and a 10% penalty. BUT there are exceptions for qualified education expenses or a first-time home purchase.

You Can’t Make Up Lost Years - Roth IRA allowances are use-it-or-lose-it. Miss the annual deadline (generally April 15th of the following year) and you lose the chance to contribute for that tax year forever.

This is obviously not for everyone, and like any investment decision you need to consider the risks carefully. I would also note that convincing a minor to voluntarily put earned income into an investment account controlled by a parent is not an easy task (and may have its' own risks, depending on the reliability of the parents). And I would highly recommend reading Sabrina Karl's suggestions about using this as a way to help develop a savings mindset in your teenagers - like offering matching deposits, or some kind of incentive program by relatives.

BUT it takes advantage of one of the most powerful tools known to man - the power of compound interest - at a times when 99% of teens are not making enough money to have to pay income taxes! So conceivably you could have tax-free deposits in your teens, and tax-free withdrawals 50-60 years later in retirement.

Articles/Resources on How This Works (starting with the original article):

"Did Your Kid Earn a Paycheck This Year? This Could Be the Most Valuable Holiday Gift You Give", Investopedia, Dec 2025, https://www.investopedia.com/did-your-kid-earn-a-paycheck-this-year-this-could-be-the-most-valuable-holiday-gift-you-give-11871440

"Custodial Roth IRA: A Roth IRA for Kids", NerdWallet, Nov 2025, https://www.nerdwallet.com/retirement/learn/why-your-kid-needs-a-roth-ira

"Roth IRA for Kids Explained", Mercer Advisors, Sep 2025, https://www.merceradvisors.com/insights/family-finance/roth-ira-for-kids-explained/

"Roth IRA Rules for Minors–How to Make Kids Millionaires" (video), Money Girl - Quick and Dirty Tips, Nov 2025, https://www.youtube.com/watch?v=Ai2WvBSXt5w

"Roth IRAs for Kids? Absolutely.", Lord Abbett, Apr 2024, https://www.lordabbett.com/en-us/financial-advisor/insights/retirement-planning/roth-iras-for-kids--absolutely-.html

"Why Every Parent Should Consider a Roth IRA for Their Child" (video), A Wiser Retirement®, Oct 2024, https://www.youtube.com/watch?v=ysjGCIroD1M

ECON and More

Curating articles for K-12 education.

CONTACT

© 2025. All rights reserved.